Personal Loans for Students with No Job:

Many students face financial challenges while pursuing their education, particularly when they lack a job to support their expenses. Personal loans for students with no job can be a viable option, allowing them to cover tuition, textbooks, and living costs. Understanding the availability and terms of these loans is crucial for students seeking financial assistance.

While traditional lenders often require proof of income, there are options specifically tailored for students entering or continuing their studies without employment. Many lenders consider a student’s future earning potential and may assess factors such as credit history and a cosigner’s support instead of income alone.

Navigating the landscape of personal loans can seem daunting, but knowledge is key. By exploring different lending institutions and understanding the application process, students can find opportunities that suit their unique situations and help them achieve their academic goals.

Understanding Personal Loans for Students

Navigating the landscape of personal loans can be complex, especially for students without a job. Key factors play a crucial role, including eligibility criteria, alternatives to traditional employment, and the influence of credit scores on loan approval.

Eligibility Criteria for Students with No Job

Students seeking personal loans without employment must be aware of specific eligibility requirements. Lenders typically assess factors such as age, educational status, and residency. Many institutions require borrowers to be at least 18 years old and enrolled in an accredited program.

Some lenders may accept a cosigner, which enhances the chances of approval. This individual should have a steady income and good credit history, effectively sharing the responsibility of the loan.

Alternatives to Traditional Employment Requirements

It is common for lenders to consider alternative means of income or financial stability. Scholarships, grants, and student stipends may serve as income sources for those without traditional jobs. Additionally, savings accounts or parental support can be factored into an application.

Peer-to-peer lending platforms sometimes waive employment requirements, providing more flexibility. Exploring these options can broaden a student’s chances of obtaining a loan.

The Role of Credit Scores in Loan Approval

Credit scores significantly influence loan approval decisions. A score above 700 is generally considered good, while anything below 600 may be categorized as bad credit. Students lacking credit history can struggle, but some lenders offer options specifically designed for them.

In cases of bad credit, personal loans may still be accessible, typically with higher interest rates. It is advisable for students to consult with loan consultants to understand their options and improve their financial standing before applying.

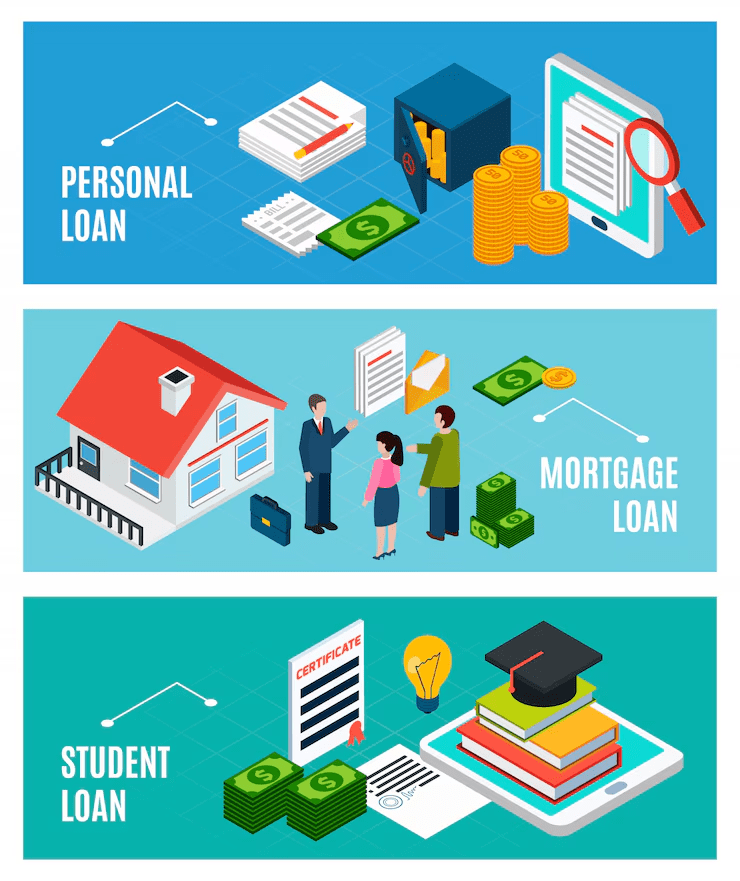

Types of Loans Available for Students

Students have access to various types of loans to help finance their education. Understanding the differences among these options can assist them in making an informed choice.

Unsecured Personal Loans

Unsecured personal loans are a common option available to students without stable income. These loans do not require collateral, meaning the borrower does not need to risk any assets. Lenders typically consider credit history, even if minimal, and may charge higher interest rates due to the added risk.

Some lenders may specifically cater to students, offering flexible terms. Before applying, students should compare rates and fees from various lenders to find the best deal. Online platforms often facilitate this process, allowing easy comparison to select favorable loan conditions.

Secured Loan Options

Secured loans require collateral, such as a vehicle or savings account. This security can lead to lower interest rates, making them an appealing option for students who might not qualify for unsecured loans. By backing the loan with an asset, the lender reduces their risk.

Students should assess the value of their collateral before pursuing this option, as failure to repay can result in loss of the asset. Institutions like banks or credit unions commonly offer these loans. It’s essential to thoroughly understand the terms and conditions before committing.

Government-Backed Loans and Schemes

Government-backed loans, such as those offered through the Pradhan Mantri Awas Yojana – Urban (PMAY(U)), provide students with favorable repayment terms and lower interest rates. These schemes often focus on making education more accessible.

Additionally, various state-specific programs, like the TS minority loan, may assist students from minority backgrounds. Such loans can bridge funding gaps without overwhelming financial burdens.

Students are encouraged to research eligibility criteria and apply promptly, as government programs may have limited availability or specific application windows.

Application Process for Student Loans

The application process for student loans involves several key steps, along with necessary documentation and an understanding of the loan terms. This ensures a smoother experience for students seeking financial assistance.

Online Application Steps

Students typically begin by visiting the lender’s website to access the loan application. They must create an account, providing personal information such as name, address, date of birth, and Social Security number.

Next, students must fill out details regarding their educational institution, field of study, and expected graduation date. It is vital to indicate any existing debts and income sources, even if they have no job.

After completing the application, students often receive a preliminary credit decision. If approved, they may need to complete additional steps to finalize their loan, including verifying their identity. Platforms like Northern Arc Capital may also offer a streamlined online application process.

Required Documentation

When applying for a student loan, several documents are typically required to process the application. Students should prepare to provide proof of enrollment, such as a letter from their educational institution.

Additional documentation may include tax returns, bank statements, and proof of income if applicable. In cases where students have no income, a co-signer might be needed, and the lender may require their financial information.

For loans from entities like Chemmanur Gold Loan, alternative forms of collateral may also be documentation. Thus, familiarity with the lender’s specific requirements is crucial.

Understanding the Fine Print

Careful attention to the terms and conditions of the loan is essential. Students should be aware of interest rates, repayment schedules, and any fees associated with the loan.

Lenders often provide an education loan sanction letter, which details the loan amount, interest, and terms. This document is crucial for understanding repayment obligations.

Moreover, awareness of variable vs. fixed interest rates can impact repayment amounts significantly. Students should ask clarifying questions to avoid unexpected costs during the repayment period.

Repayment Strategies for Students

Managing repayment of student loans can be a complex process, especially for those without a steady income. Focusing on personalized repayment strategies, loan forgiveness options, and effectively handling multiple loans can significantly aid in a smoother repayment journey.

Creating a Repayment Plan

A detailed repayment plan is essential for students. A budget should include income sources like part-time work, grants, or savings. Students can use the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings or loan repayment.

Utilizing online calculators can help estimate monthly payments based on interest rates and loan terms. Students must prioritize loans with higher interest rates. Regular reviews of the repayment plan can help address any changing financial situations, enabling timely adjustments if circumstances change.

Loan Forgiveness and Deferment Options

Several programs exist that may offer loan forgiveness for qualifying students. For instance, public service roles can lead to forgiveness after a specific number of payments. It’s crucial to research eligibility criteria for each program.

Deferment options allow students to temporarily postpone payments without penalties. This can be beneficial for those who face financial hardships. Specific types of loans, such as a handicapped loan, may offer unique deferment opportunities worth exploring. Understanding these options provides students with the flexibility they may need during challenging times.

Managing Multiple Student Loans

Managing multiple loans can be overwhelming. Consolidation is a viable option that combines several loans into one, simplifying payments and potentially lowering interest rates. Students should analyze both federal and private consolidation options to understand the trade-offs.

Using an organized tracking system, like a spreadsheet, helps keep payment dates and amounts clear. Students must also consider income-driven repayment plans. These plans adjust monthly payments based on income, providing financial relief for those with limited earnings after graduation.

Utilizing these strategies effectively can contribute to a manageable repayment experience for students.

Financial Management for Students

Effective financial management is essential for students, especially those who may not have a steady income. Building a good credit history, investing wisely, and budgeting for expenses are key strategies that can lead to long-term financial stability.

Building a Good Credit History

Establishing a solid credit history is vital for students, particularly when applying for personal loans. One effective method is to obtain a credit card specifically designed for students. These cards often come with lower credit limits but help in building positive credit history.

To raise a credit score quickly, it’s important to pay bills on time and keep credit utilization low, ideally below 30%. Regularly monitoring credit reports can also help identify discrepancies or issues that may hinder credit scores.

Investment Tips and Education

Investing can be a valuable way for students to grow their finances. Options such as the Mahila Samman Savings Certificate offer attractive interest rates, making them a good choice for saving. Generally, students should educate themselves on various investment avenues like stocks, bonds, or even precious metals.

Is gold a good investment? Historically, gold can serve as a hedge against inflation. However, students must conduct thorough research to determine if it fits their financial goals and risk tolerance.

Budgeting and Savings for Loan Repayment

Creating a budget is crucial for managing expenses while studying. Students should start by listing all income sources and fixed expenditures such as rent, utilities, and food. This can be complemented by tracking variable expenses to understand spending patterns.

To prepare for loan repayment, students should allocate a portion of their budget towards savings. Establishing an emergency fund can also help mitigate unexpected expenses, making repayment more manageable. By planning strategically, students can avoid financial pitfalls and ensure they remain on track with their obligations.

Loan Products and Services

Various loan products are available for students without a job, focusing on flexibility and accessibility. Understanding the nuances of these options can help in making informed decisions.

Comparing Interest Rates and Fees

Interest rates and fees vary significantly among different lenders. Students should be diligent in comparing these costs before selecting a loan.

- Instant Payday Loans: These loans often come with high fees and APRs. While fast, they can lead to difficulty in repayment.

- Bakri Palan Loan: Typically offers moderate interest rates, making it an attractive option compared to payday loans.

- Cooperative Bank Loan Interest Rates: These loans may offer competitive rates, especially for students, but often require membership in the bank.

- Gramin Bank Gold Loan Interest Rate: This option entails lower interest rates if collateral is provided, adding a layer of security for lenders.

Students should carefully consider these factors to find the best possible terms for their financial situation.

Innovative Loan Apps and Digital Platforms

Digital platforms and innovative apps are becoming prominent in the lending landscape. They offer streamlined applications and quick approvals.

- Orabora Loans: Known for its easy online application process, it can provide necessary funds quickly.

- BharatPe Loan Eligibility: Simplifies access to loans for students by using digital profiles rather than traditional credit scores.

- Motilal Oswal Home Loan: Though typically aimed at homebuyers, their digital approach is useful for understanding loan terms and conditions.

Using these platforms can enhance the borrowing experience, making it less cumbersome for students.

Financial Institutions and Loan Providers

Various financial institutions offer tailored services for student loans. Understanding the options can simplify the decision-making process.

- Daily Collection Loan: This service focuses on small, manageable payments often suitable for students.

- JK Bank Housing Loan Interest Rate: While aimed at homebuyers, students may qualify if they have a stable financial history.

- JM Financial Home Loans Limited: Specializes in loans with flexible repayment options, ideal for students anticipating future employment.

- Keerthana Gold Loans: Offers loans against gold, allowing students to secure funding without a job.

Investigating these institutions can unveil suitable options for students, promoting financial wellness.

Risks and Considerations

When considering personal loans for students with no job, it’s crucial to understand potential risks and responsibilities. Students should be aware of predatory lending practices, the consequences of defaulting on loans, and the importance of managing debt responsibly.

Understanding Loan Predatory Practices

Predatory lending practices can significantly impact students seeking loans. These practices include high interest rates, excessive fees, and misleading terms. For instance, payday loans in Bangalore and rapid loans often target vulnerable borrowers, including students.

Both types of loans may come with extremely high interest rates, making repayment challenging. Students should thoroughly research lenders and look for reputable companies offering fair terms. It’s essential to read all agreements carefully and ask questions before signing any contract.

The Impact of Defaulting on Loans

Defaulting on a loan can lead to severe financial consequences. Students without jobs may struggle to meet repayment deadlines, putting them at risk of default. This situation can result in negative credit scores, making future borrowing more difficult.

In addition, lenders may engage in aggressive collection practices. This might include wage garnishment or even legal action.

Understanding the long-term effects of defaulting is vital for students weighing their options. They should assess their financial situation and consider whether they can realistically repay the loan before proceeding.

Managing Debt Responsibly

Effective debt management requires careful planning and discipline. Students should first create a realistic budget that includes their income and expenses. Using budgeting tools can help them track their finances more effectively.

They can also explore alternatives to loans, such as scholarships or part-time jobs. For students considering loans, it’s important to borrow only what is necessary, especially when options like salary advance loans without CIBIL checks might seem appealing yet risky.

Additionally, students should be informed about loan repayment plans and potential assistance programs, like the farmer loan redemption scheme in Uttar Pradesh. Staying proactive in financial planning helps ensure students can manage their debt effectively while pursuing their education.